Summary

Oil prices are one of the most discussed issues in economics. The Organization of the Petroleum Exporting Countries (OPEC) plays an important role in oil markets as their production targets affect oil prices. The OPEC and the U.S. government have generated forecasts showing higher demand and lower supply for crude. With the U.S. producing less due to the suspension of oil rigs in operation and thus consuming more, the OPEC reported that demand for its petroleum will rise. Moreover, the U.S. Energy Information Administration reported a forecast stating that there would be a slower production growth in six of the primary seven shale plays in the U.S. causing the U.S. benchmark to settle at $52.86 a barrel, increasing up 19% since its low hit. The settlement of Brent Crude at $58.34 a barrel has also increased the global benchmark up 25% from the low. If oil prices were to be sustained, rising crude prices would help restraint the greatly low petroleum prices that the U.S. consumers have benefited from the last few months. However, rising oil prices could also land a negative impact on the already-struggling global economy. The stabilization in gasoline prices may also be tough to achieve as demand in China is low which may lead to an oversupply in the oil market.

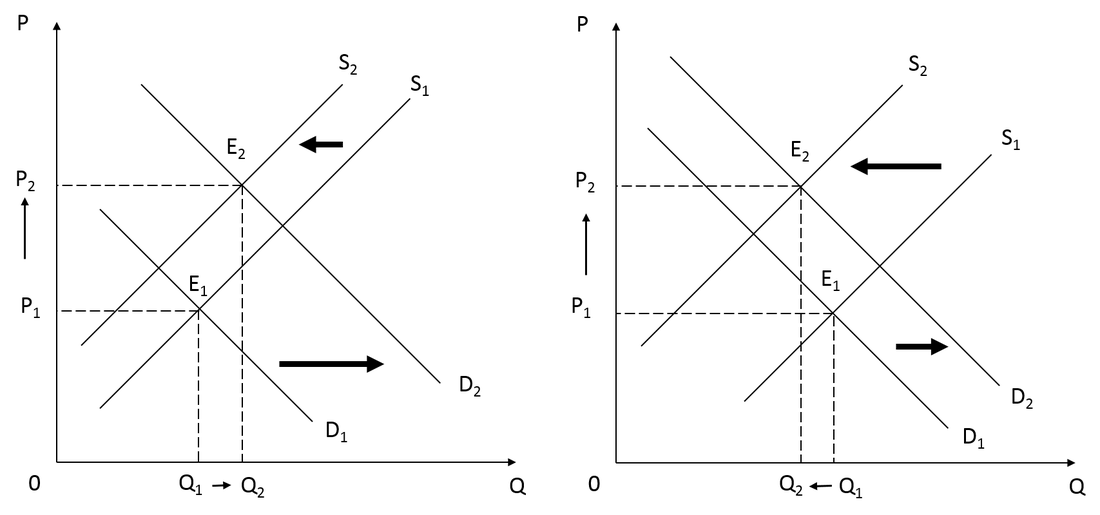

Market Equilibrium

In the commerce market, demand and supply come together to form an interaction between buyers and sellers in order to determine what goods and services to produce and the prices of them. When the demand curve and the supply curve are brought together, an equilibrium price will be achieved when both curves intersect each other. However, oil prices are not in equilibrium as forecasts from the OPEC and the U.S. government show signs of higher demand and lower supply for crude oil. “A wave of spending cuts by oil producers and a sharp decline in the number of rigs drilling for crude in the U.S. likely will slow the nation’s oil-output growth” (Kent and Faucon, 2015) and thus increasing the demand for OPEC’s crude oil. Even though U.S. oil producers have cut down in production, U.S. consumers are consuming more. As stated in the forecasts provided by OPEC and the U.S., with an increased demand, supply will generally be lower.

Elasticity

Gasoline prices are constantly fluctuating due to various reasons. Different types of consumers react differently to changes in the price of oil. For some people, they claimed that “consumers don’t vary the quantity of gas they buy as the price fluctuates because the number of miles they need to drive to get to work or school or to run errands is roughly constant” ((Hubbard and O'Brien, 2015)). However in actual reality, many consumers actually seek ways to cut back on the gasoline they purchase. Price elasticity differs as well in the short run and the long run. In the short run, price elasticity seems to be quite low where there is not much change in demand with a change in price. Most consumers have cars that commit them to a certain type of crude oil. Therefore, it limits their responses and behavior on changes in gasoline prices giving a low price elasticity of demand in the short run. On the other hand, in the future, technology will be even more improved and advanced and the automotive industries will be able to produce more affordable fuel efficient cars. Therefore in the long run, there may be more consumers who own fuel efficient cars or consumers may have other options to commute to places, which do not limit consumers in responding to changes in crude prices causing price elasticity for demand to be higher. Aside from the fact that U.S. oil producers are producing less, OPEC reported a rise in demand for its crude is because U.S. consumers are still consuming and are consuming more since U.S. oil producers have cut down on their oil production. For oil producers, the price elasticity for supply varies as well in the short run and the long run. During the previous months, U.S. consumers have benefited from the lower gasoline prices. Although it has caused negative impacts on suppliers’ profits, it is more rational for suppliers to keep its business going rather than shutting it down in the short run as producers may suffer a greater loss. Therefore price elasticity for supply in the short run is quite low as well. According to Barclays PLC and Citigroup Inc., “rig cuts won’t lead to production cuts, and prices will have room to fall back as storage fills up and their supplies go back on to the market” (Puko and Erheriene, 2015). Whereas in the long run, it will depend on the decisions and strategies that producers make and come up with in order to determine its price elasticity for supply in the long run.

Price Ceiling or Price Floor

The crude prices settlement of the U.S. benchmark and the global benchmark have increased 19% up and 25% up from the low respectively thus the price ceiling or price floor for crude prices are expected to have a new range of $40 to $50. Many analysts suggest the range to be a price floor “because positioning in the futures market suggests expectations of a fairly quick rebound to $70 or $80” (Kaletsky, 2015). However, due to the history of adjusted oil prices caused by inflation and the constant fluctuation of oil prices, economists suggest the range to be a price ceiling instead and that “today’s price should be viewed as a probable ceiling for a much lower trading range, which may stretch all the way down toward $20” (Kaletsky, 2015). Reason being for the new expected trading range to be as low as $20 is that crude demand will decrease in the long term following the evolution of technology and geology. This could result in high-cost crude being devalued. “Although shale oil is relatively costly, production can be turned on and off much more easily and cheaply than from conventional oil fields” (Kaletsky, 2015). This gives the U.S. shale producers the advantage to gain “swing producers” status in the global oil industries thus causing the OPEC to lose its ability to set crude prices. In a competitive oil industry, low-cost crude producers would choose to keep its business going no matter what the demand is, whereas shale productions are able to choose to operate or suspend their rigs operations depending on the market demand. With this logic, Kaletsky concluded that “marginal costs of American shale oil, generally estimated at $40 to $50 a barrel, should in the future be a ceiling for global oil prices, not a floor” (Kaletsky, 2015).

Demand and supply are basically what decide the prices of a certain product or service in the commerce world. Demand and supply relate closely to each other as they are indications on how to determine what kind of product or service a company should provide in order to meet society’s demands and the prices of them. The OPEC and the U.S. government have released forecasts showing that crude prices will rise for a higher demand and a lower supply. With the U.S. oil production growth being reduced, OPEC reported that its crude oil will generally increase. “OPEC estimates that demand will grow to 29.2 million barrels a day, 100,000 more than a year ago.” (Puko and Erheriene, 2015). When the demand curve and the supply curve come together and intersect each other, market equilibrium will be achieved. “Once a market is in equilibrium, it remains in equilibrium” (Hubbard and O’Brien, 2015) where the demand curve and the supply curve remain unchanged. However, shifting along the curves or quantity demanded and quantity supplied would result in surplus and shortage. The occurrence of a surplus happens when quantity supplied is greater than quantity demanded whereas the occurrence of a shortage happens when quantity demanded is greater than the quantity supplied. China is the second largest consumer of crude oil. However, its demand is down which if it were to carry on in the future, it “would increase the oversupply on the oil market and make it more difficult for oil prices to recover further” (Puko and Erheriene, 2015). In order to avoid surpluses, most companies would cut prices in order to increase quantity demanded and decrease quantity supplied. However, if the company still sets the price above the price equilibrium, there will still be a surplus and if the price falls to the equilibrium price only will the market achieve equilibrium.

In Conclusion, being able to understand and apply economic concepts are vital for business markets and industries to succeed. Crude oil are one of the most important issues in economics as its prices are constantly fluctuating. Oil is one the natural resources that our planet is running out and people very much depend on it because there are many things that are oil-derived. Therefore it is significant to understand about economic concepts in order to avoid surpluses or shortages.

Reference List

1. Kent, S. and Faucon, B. (2015). Oil-Price Rebound Predicted. [online] WSJ. Available at: http://www.wsj.com/articles/demand-for-opec-crude-will-rise-this-year-says-group-1423482563 [Accessed 7 Jun. 2015].

2. Hubbard, R. and O'Brien, A. (2015). Economics. 5th ed. Pearson Education Limitted, p.233.

3. Puko, T. and Erheriene, E. (2015). Oil Rises on Optimism For Higher Demand, Lower Supply. [online] WSJ. Available at: http://www.wsj.com/articles/crude-rises-on-opec-forecast-of-increased-demand-1423485545?cb=logged0.17587351240217686 [Accessed 7 Jun. 2015].

4. Kaletsky, A. (2015). What is the future direction of oil prices? | Anatole Kaletsky. [online] the Guardian. Available at: http://www.theguardian.com/business/2015/jan/15/what-is-the-future-direction-of-oil-prices-anatole-kaletsky [Accessed 7 Jun. 2015].

5. Kaletsky, A. (2014). Finding the Floor, or Ceiling, for Oil Prices. [online] Nytimes.com. Available at: http://www.nytimes.com/2014/12/19/business/international/finding-the-floor-or-ceiling-for-oil-prices.html?_r=0 [Accessed 7 Jun. 2015].

Oil prices are one of the most discussed issues in economics. The Organization of the Petroleum Exporting Countries (OPEC) plays an important role in oil markets as their production targets affect oil prices. The OPEC and the U.S. government have generated forecasts showing higher demand and lower supply for crude. With the U.S. producing less due to the suspension of oil rigs in operation and thus consuming more, the OPEC reported that demand for its petroleum will rise. Moreover, the U.S. Energy Information Administration reported a forecast stating that there would be a slower production growth in six of the primary seven shale plays in the U.S. causing the U.S. benchmark to settle at $52.86 a barrel, increasing up 19% since its low hit. The settlement of Brent Crude at $58.34 a barrel has also increased the global benchmark up 25% from the low. If oil prices were to be sustained, rising crude prices would help restraint the greatly low petroleum prices that the U.S. consumers have benefited from the last few months. However, rising oil prices could also land a negative impact on the already-struggling global economy. The stabilization in gasoline prices may also be tough to achieve as demand in China is low which may lead to an oversupply in the oil market.

Market Equilibrium

In the commerce market, demand and supply come together to form an interaction between buyers and sellers in order to determine what goods and services to produce and the prices of them. When the demand curve and the supply curve are brought together, an equilibrium price will be achieved when both curves intersect each other. However, oil prices are not in equilibrium as forecasts from the OPEC and the U.S. government show signs of higher demand and lower supply for crude oil. “A wave of spending cuts by oil producers and a sharp decline in the number of rigs drilling for crude in the U.S. likely will slow the nation’s oil-output growth” (Kent and Faucon, 2015) and thus increasing the demand for OPEC’s crude oil. Even though U.S. oil producers have cut down in production, U.S. consumers are consuming more. As stated in the forecasts provided by OPEC and the U.S., with an increased demand, supply will generally be lower.

Elasticity

Gasoline prices are constantly fluctuating due to various reasons. Different types of consumers react differently to changes in the price of oil. For some people, they claimed that “consumers don’t vary the quantity of gas they buy as the price fluctuates because the number of miles they need to drive to get to work or school or to run errands is roughly constant” ((Hubbard and O'Brien, 2015)). However in actual reality, many consumers actually seek ways to cut back on the gasoline they purchase. Price elasticity differs as well in the short run and the long run. In the short run, price elasticity seems to be quite low where there is not much change in demand with a change in price. Most consumers have cars that commit them to a certain type of crude oil. Therefore, it limits their responses and behavior on changes in gasoline prices giving a low price elasticity of demand in the short run. On the other hand, in the future, technology will be even more improved and advanced and the automotive industries will be able to produce more affordable fuel efficient cars. Therefore in the long run, there may be more consumers who own fuel efficient cars or consumers may have other options to commute to places, which do not limit consumers in responding to changes in crude prices causing price elasticity for demand to be higher. Aside from the fact that U.S. oil producers are producing less, OPEC reported a rise in demand for its crude is because U.S. consumers are still consuming and are consuming more since U.S. oil producers have cut down on their oil production. For oil producers, the price elasticity for supply varies as well in the short run and the long run. During the previous months, U.S. consumers have benefited from the lower gasoline prices. Although it has caused negative impacts on suppliers’ profits, it is more rational for suppliers to keep its business going rather than shutting it down in the short run as producers may suffer a greater loss. Therefore price elasticity for supply in the short run is quite low as well. According to Barclays PLC and Citigroup Inc., “rig cuts won’t lead to production cuts, and prices will have room to fall back as storage fills up and their supplies go back on to the market” (Puko and Erheriene, 2015). Whereas in the long run, it will depend on the decisions and strategies that producers make and come up with in order to determine its price elasticity for supply in the long run.

Price Ceiling or Price Floor

The crude prices settlement of the U.S. benchmark and the global benchmark have increased 19% up and 25% up from the low respectively thus the price ceiling or price floor for crude prices are expected to have a new range of $40 to $50. Many analysts suggest the range to be a price floor “because positioning in the futures market suggests expectations of a fairly quick rebound to $70 or $80” (Kaletsky, 2015). However, due to the history of adjusted oil prices caused by inflation and the constant fluctuation of oil prices, economists suggest the range to be a price ceiling instead and that “today’s price should be viewed as a probable ceiling for a much lower trading range, which may stretch all the way down toward $20” (Kaletsky, 2015). Reason being for the new expected trading range to be as low as $20 is that crude demand will decrease in the long term following the evolution of technology and geology. This could result in high-cost crude being devalued. “Although shale oil is relatively costly, production can be turned on and off much more easily and cheaply than from conventional oil fields” (Kaletsky, 2015). This gives the U.S. shale producers the advantage to gain “swing producers” status in the global oil industries thus causing the OPEC to lose its ability to set crude prices. In a competitive oil industry, low-cost crude producers would choose to keep its business going no matter what the demand is, whereas shale productions are able to choose to operate or suspend their rigs operations depending on the market demand. With this logic, Kaletsky concluded that “marginal costs of American shale oil, generally estimated at $40 to $50 a barrel, should in the future be a ceiling for global oil prices, not a floor” (Kaletsky, 2015).

Demand and supply are basically what decide the prices of a certain product or service in the commerce world. Demand and supply relate closely to each other as they are indications on how to determine what kind of product or service a company should provide in order to meet society’s demands and the prices of them. The OPEC and the U.S. government have released forecasts showing that crude prices will rise for a higher demand and a lower supply. With the U.S. oil production growth being reduced, OPEC reported that its crude oil will generally increase. “OPEC estimates that demand will grow to 29.2 million barrels a day, 100,000 more than a year ago.” (Puko and Erheriene, 2015). When the demand curve and the supply curve come together and intersect each other, market equilibrium will be achieved. “Once a market is in equilibrium, it remains in equilibrium” (Hubbard and O’Brien, 2015) where the demand curve and the supply curve remain unchanged. However, shifting along the curves or quantity demanded and quantity supplied would result in surplus and shortage. The occurrence of a surplus happens when quantity supplied is greater than quantity demanded whereas the occurrence of a shortage happens when quantity demanded is greater than the quantity supplied. China is the second largest consumer of crude oil. However, its demand is down which if it were to carry on in the future, it “would increase the oversupply on the oil market and make it more difficult for oil prices to recover further” (Puko and Erheriene, 2015). In order to avoid surpluses, most companies would cut prices in order to increase quantity demanded and decrease quantity supplied. However, if the company still sets the price above the price equilibrium, there will still be a surplus and if the price falls to the equilibrium price only will the market achieve equilibrium.

In Conclusion, being able to understand and apply economic concepts are vital for business markets and industries to succeed. Crude oil are one of the most important issues in economics as its prices are constantly fluctuating. Oil is one the natural resources that our planet is running out and people very much depend on it because there are many things that are oil-derived. Therefore it is significant to understand about economic concepts in order to avoid surpluses or shortages.

Reference List

1. Kent, S. and Faucon, B. (2015). Oil-Price Rebound Predicted. [online] WSJ. Available at: http://www.wsj.com/articles/demand-for-opec-crude-will-rise-this-year-says-group-1423482563 [Accessed 7 Jun. 2015].

2. Hubbard, R. and O'Brien, A. (2015). Economics. 5th ed. Pearson Education Limitted, p.233.

3. Puko, T. and Erheriene, E. (2015). Oil Rises on Optimism For Higher Demand, Lower Supply. [online] WSJ. Available at: http://www.wsj.com/articles/crude-rises-on-opec-forecast-of-increased-demand-1423485545?cb=logged0.17587351240217686 [Accessed 7 Jun. 2015].

4. Kaletsky, A. (2015). What is the future direction of oil prices? | Anatole Kaletsky. [online] the Guardian. Available at: http://www.theguardian.com/business/2015/jan/15/what-is-the-future-direction-of-oil-prices-anatole-kaletsky [Accessed 7 Jun. 2015].

5. Kaletsky, A. (2014). Finding the Floor, or Ceiling, for Oil Prices. [online] Nytimes.com. Available at: http://www.nytimes.com/2014/12/19/business/international/finding-the-floor-or-ceiling-for-oil-prices.html?_r=0 [Accessed 7 Jun. 2015].

RSS Feed

RSS Feed